Baby steps

The Bank of England has now increased interest rates in both of its last two meetings, taking base rates to 0.5%. The 10 year gilt yield has also moved up and is now over 1.0%.

These are still vanishingly thin levels of interest by any standard. The UK equity market yields much more than cash at 3.1% and the Slater Income Fund more again, with a yield of 4.3%. We still live in the bizarre world where equities yield much more than bonds, despite the high probability that dividends will grow over time and the certainty that bond coupons will not. Rates would have to move up a lot more for the income hungry to start switching out of equities and into bonds or cash deposits.

Inflation, Rotation

In November 2021 the Chair of the US Federal Reserve observed that it was no longer appropriate to talk of inflation as “transitory”. Since then markets have been trying to gauge the extent and pace of future interest rate increases. We may come to see November as marking the end of a speculative phase in markets, the day that free money died. Even the first baby steps towards normalisation have inflicted massive pain on the areas of greatest excess, such as SPAC’s, crypto’s, meme stocks and non-profitable tech stocks.

Ultra low interest rates have supported all assets. That was the point of the policy. But the arithmetic of the time value of money means that low rates are especially beneficial for the share prices of companies whose best days are far in the future. In its extreme form this has fuelled enthusiasm for companies that make no money at all currently, let alone pay a dividend. This has been a tough environment for the equity income investor. But there are signs, concurrent with the step up in rates, that this is beginning to change.

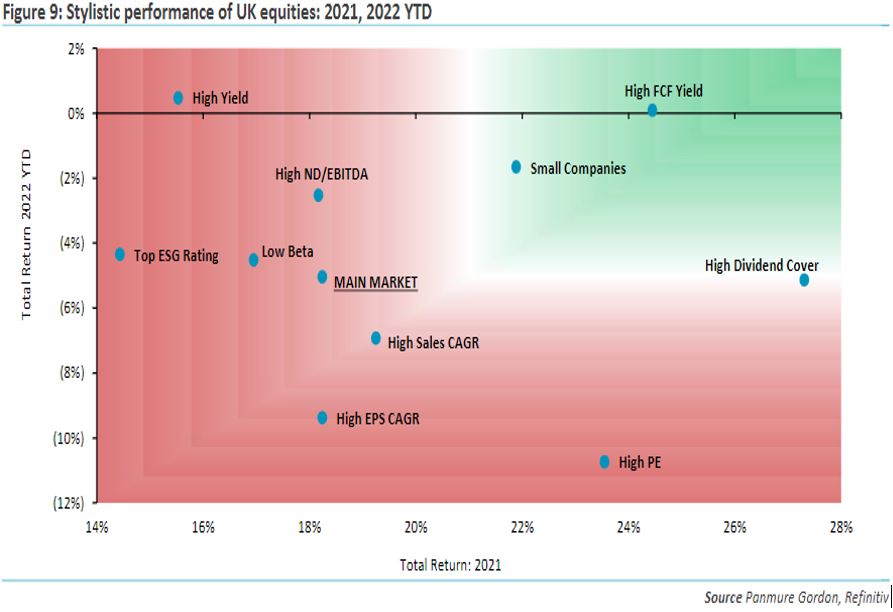

This chart shows the returns within the UK equity market of various characteristics (such as high sales growth) and how these categories, or styles, performed in 2021 (across the bottom axis) and how they have done so far in 2022 (against the side). This shows that high PE stocks led the charge in 2021 but are tailed off in 2022. High yield, by contrast, was a relative laggard in 2021 but has been a relative winner in 2022. Rotation in action.

It is noteworthy that ‘High Free Cash Flow Yield’, an important metric for our work on all our funds at Slater Investments, has been a winner in both periods. The fact that ‘Small Companies” is in the green zone on the chart is also encouraging for our multi-cap approach.

A false dawn or a glorious sunrise?

This tentative rotation will only be sustained if base rates continue to rise and the yield curve continues to steepen. The good news is that the chances of this are excellent. Interest rates are still at emergency levels, whilst the world is recovering. The OECD forecast that global growth in 2022 will be 4.5% and for a change the UK will be a bit ahead of the average. Additionally, inflation is running at 5% in the UK (and 7% in America). So nominal growth is pushing 9%, in which case bond yields of 1% make no sense.

Britannic Bounce?

It is well known that the UK has been a dreary market over the last five years compared to the exceptional returns abroad and particularly in the USA. Untangling the causes of this is tricky and Brexit must be a part of it. But a lot is compositional: the UK indices are full of resource companies and banks whilst the USA is the cradle of tech. The UK market’s biggest constituents include Unilever, HSBC and Shell whilst the American’s have Microsoft, Apple and Amazon. And well done them. But if the change in monetary regime supports a continuation of the rotation we have seen so far in 2022, then this could be encouraging for UK equities in a global context. Perhaps, not quite Cool Britannia but we might find that it’s hip to be square.

Important: Slater Investments Limited does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this article should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.