At Slater Towers we receive polite letters from companies explaining why they think it right and proper to increase the size of awards to their directors. Nil cost shares worth 1.25x base salary? Come, come, surely 1.5x is only fair? One such came through a couple of days ago. It was from a company which has risen over 50% in the last year. It sounds churlish even to purse the lips and exhale a slight hmmm.

Options costs are a real bugbear with us because many companies pretend they don’t exist. They add back the option charge to their adjusted numbers, which are nearly always so much more attractive than the, er actual ones. For us this becomes a nuisance as we do use metrics such as PE (Price/Earnings) and PEG (PE/Growth ratio) etc in our early filtering process. The problem is that some companies are diverting a large proportion of their profits towards share options while for others, typically larger ones, the leakage is not that important. Again some companies include the cost in their headline numbers while the offenders leave them out.

Imagine a company that issues the same amount of free shares, a.k.a nil cost options, to its executives each year. The accounting standard works out what the options would have cost to buy and includes a charge in the results. It also adds the soon to be created shares to the issued shares in order to work out the fully diluted earnings per share.

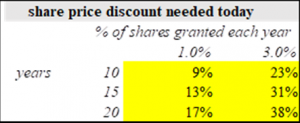

Suppose a company makes the same level of award every year. After 10, 15 and 20 years:

The figures assume that valuations remain constant over the investment period, so the only difference is the rate of share leakage. If this a bit complicated, then make life simpler by valuing companies on their earnings per share after the options charge. Apply a reasonable multiple to the true earnings and you have your price target.

Companies argue that options are important – and they certainly are to the recipients. For shareholders there may also be more dynamic performance. Maybe. As we said at the start of this piece, it’s hard to wag a finger of complaint at executive pay when a company has done well. And when it’s done badly, investors are also usually generous to incoming managements who promise to right the ship. This is a tricky subject, but let’s at least be honest about the true cost.

Important: Slater Investments Limited does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this article should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.