“Do you know the only thing that gives me pleasure? It’s to see my dividends coming in”.

Most modern income fund managers, whilst quietly agreeing with these words attributed to John D Rockefeller, would perhaps add that a growing dividend is especially pleasurable. To that end, most income investors seek out companies that provide a rising income stream rather than just a high static yield. A good and growing dividend is the mantra.

Assuming markets are even loosely efficient, we should expect a trade-off between dividend yield and dividend growth. At Slater Investments we are always looking for those anomalies that have great yield and great growth, but these situations are the exception in the stock market, not the rule. Most of the time investors sacrifice immediate yield for the prospect of growth in dividends. How can we weigh the competing charms?

Or which would you rather own

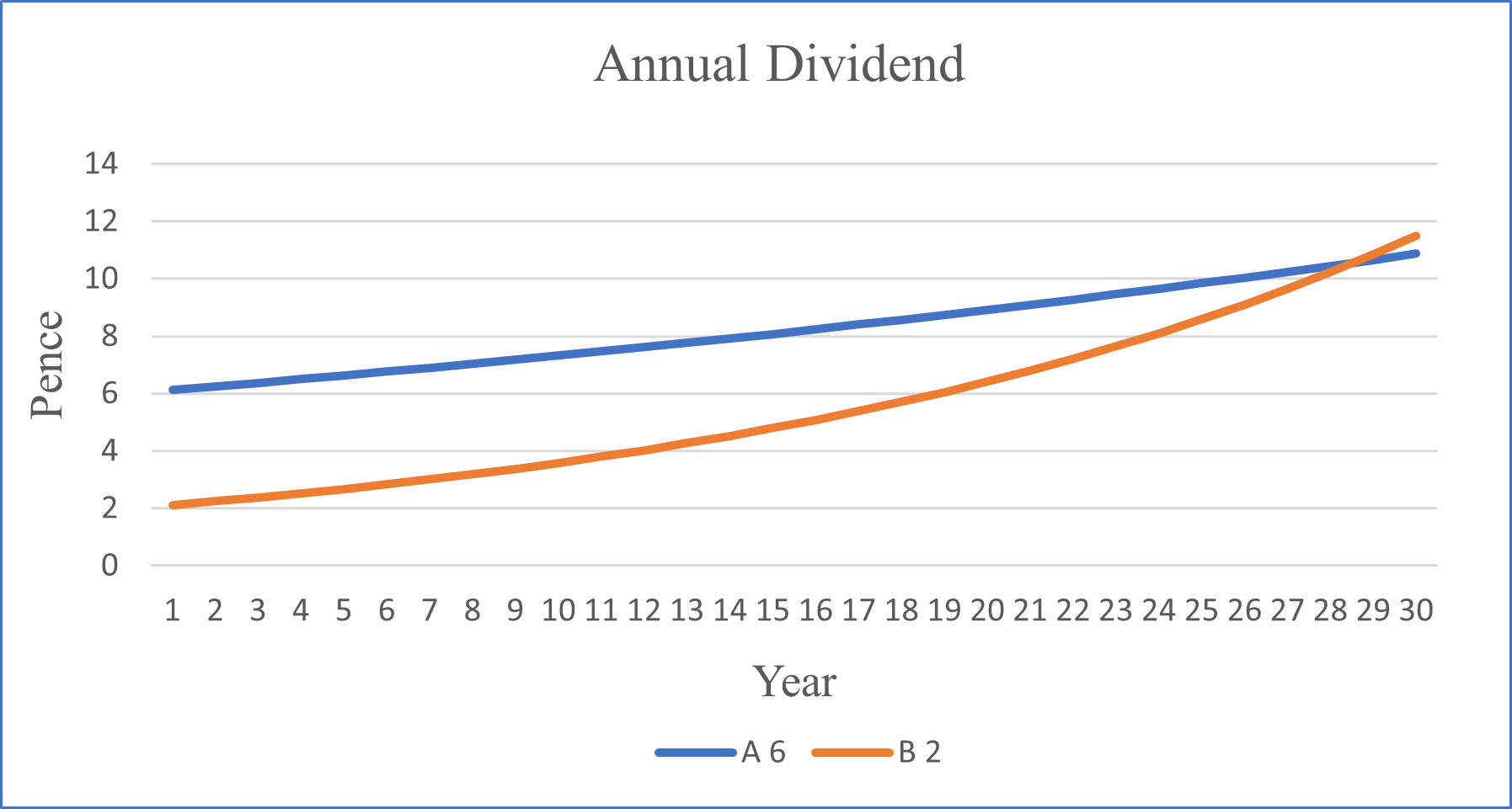

Company A: yielding 6%, growing its dividend at 2% or

Company B: yielding 2% but growing at 6%?

A pleasure-maximising Mr Rockefeller would probably plump for ‘A’ but would he be right?

One way to think about this is to model the dividends into the future, as in the chart below. The blue line is Company A, starting at 6p, growing at 2% and the red line is Company B, 2p growing at 6%.

Remarkably it is not until year 30 that Company B catches up. Even for long-term investors such as Slater Investments, 30 years is stretching the investment horizon.

Another way of making the same point is to examine how many years it would take to get one’s initial investment repaid through the dividends received. For Company A, the payback period would be somewhere between 13 and 14 years but for the lower yielding but faster growing Company B, it would take nearly 23 years to be repaid.

This is even more acute if we make some allowance for the time value of money…6p today is worth more than 6p in 19 years’ time. We could allow for this by applying a discount rate to the future cashflows. Applying a 5% discount rate to both cash flow series means the payback period is pushed out for both shares. For Company A the payback on a discounted basis would be 21 years but for Company B it would take a longevity defying 40 to be repaid through the dividend stream.

So, perhaps a bird in the hand is indeed worth two in bush. Take the higher yield, embrace your inner Rockefeller, and enjoy the pleasure of those dividends coming in.

What this ignores, of course, is how we might expect the share prices of the two theoretical companies to perform over the years. This is something we will expand on in our next “Dividend Watch”. Stay tuned!

Important: Slater Investments Limited does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this article should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.