Dividend cover is a simple calculation to provide investors with an idea of whether companies are paying dividends that they can afford. The calculation looks at the ratio of a company’s net income to the total dividend paid to shareholders. Put simply, if a company has a net income of £10m and they pay out £5m in dividends, the dividend cover ratio will be 2. Or it can be expressed at a per share level: a 5p dividend from 10p of earnings per share (EPS) is similarly twice covered.

A decent level of cover is desirable for two reasons. Firstly, it suggests that the company could still support the dividend if there were a bump in the road and net income fell. More positively, a well covered dividend means the company is not over-distributing but is retaining some of its profits for re-investment in the business. This is good because it supports dividend growth in the longer-term.

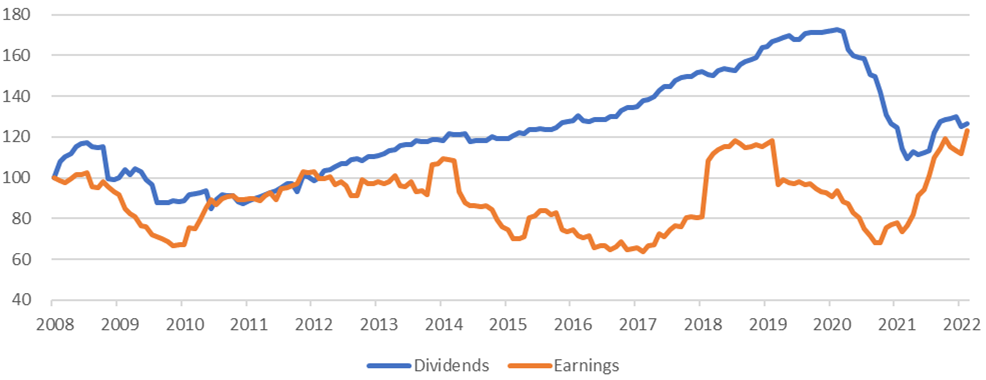

The chart below shows the performance of both the dividends and earnings of the wider UK Equity market, rebased to 100, from 2008 to 2020. An income investor’s dream is to see the blue and orange line rise in tandem as they did between mid-2010 to 2012. But since then dividends kept rising but this was not supported by growth in earnings.

Source: Slater Investments

This persisted because in aggregate managements kept juicing the dividends in anticipation of a recovery in earnings, a recovery which never materialised. This meant that the UK market has been guilty of over-distributing.

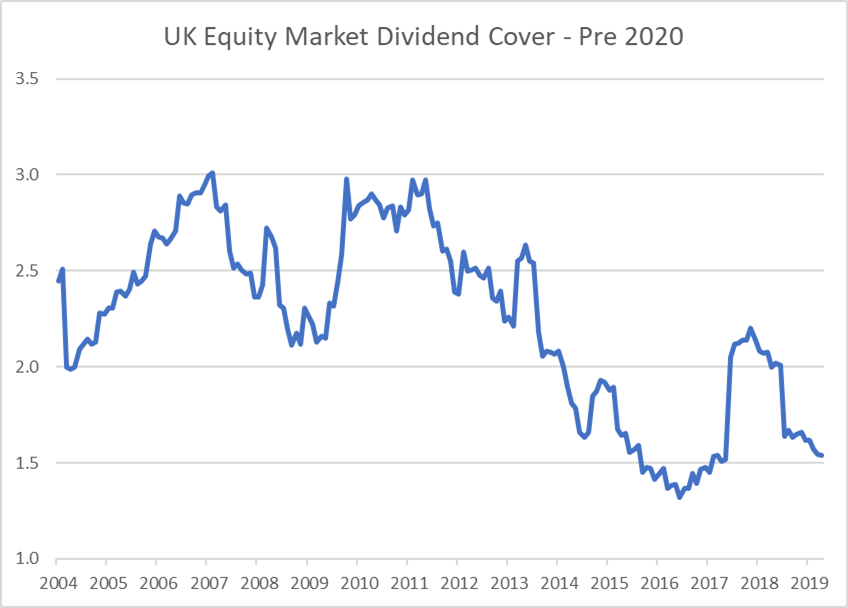

As a result dividend cover got thinner and thinner, falling below 1.5x by 2019.

Source: Slater Investments

Maybe this over-distribution and the associated lack of re-investment is a contributory factor to the lack of productivity growth in the UK.

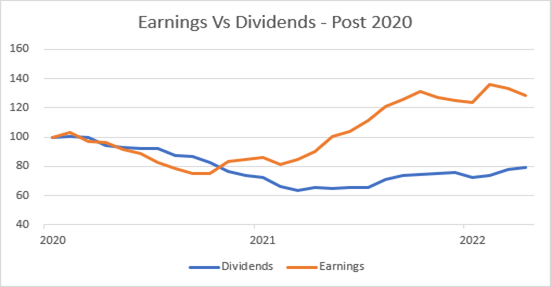

Then there was Covid. In 2020 the UK market saw the most ferocious and wide spread dividend cuts. The Link Dividend Monitor estimate that total distributions fell 43%. This made the Global Financial Crisis look like a tea party. And unlike the GFC, dividends fell much more deeply than earnings.

Source: Slater Investments

Since restrictions have eased, the UK’s overall economic output has recovered to pre-Covid levels. As have overall corporate earnings. But, as the chart above shows, dividends have been restored at a much more cautious rate. Human nature plays its part here. It has been traumatic for boards to cut their dividends. It is not something they ever want to have to do again. So, when coming to restore their dividends they have pitched them at cautious levels.

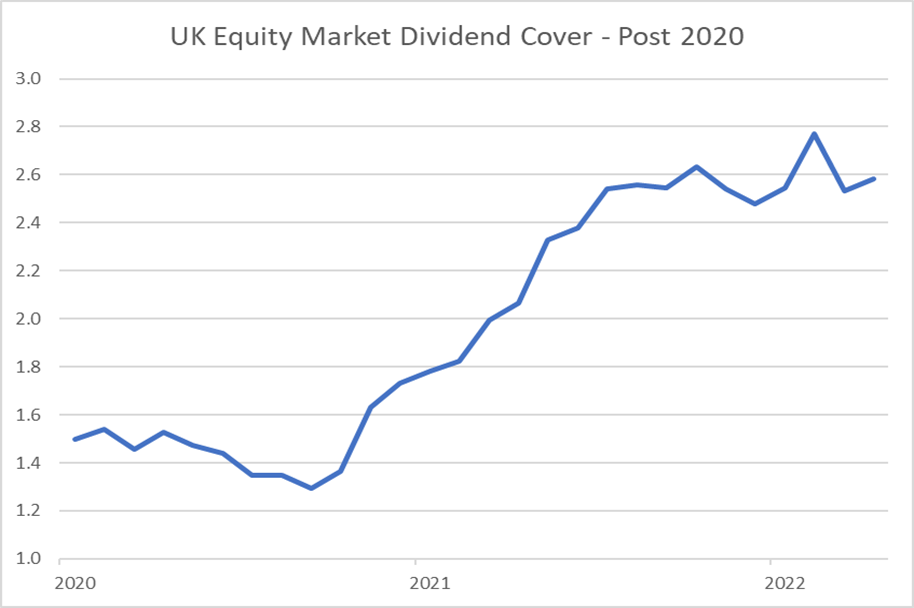

This is where the good news comes in because it means that dividend cover has been much improved.

Source: Slater Investments

In fact dividend cover is back to levels not seen since the credit crunch. This means equity investors can feel more confident that their dividends are secure and that even if there are a few bumps in the road, the restored level of cover should act as a shock absorber.

This significant reset is another reason to be confident about the dividend prospects for the Slater Income Fund.

Important: Slater Investments Limited does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this article should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.