In Pride and Prejudice Mrs Bennet exclaimed about Mr Darcy: ‘..what jewels, what carriages you will have…Ten thousand a year! Oh, Lord! What will become of me. I shall go distracted.’ If Mr Darcy turned up today armed only with £10,000 he would come with a plastic earing in one ear and jingling the keys to an old banger.

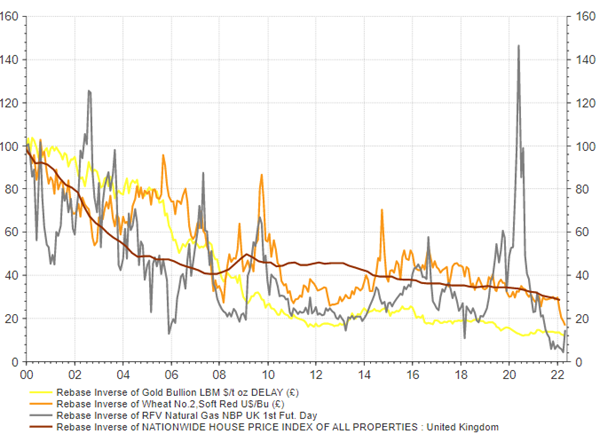

Never mind two centuries of debasement, we only need to look back a couple of decades to see the same trend hard at work. Rebased to 100, the chart below tracks how much gold, gas, wheat and housing the same amount of pounds sterling would now buy. Five gold rings? Make that one, and probably only gold-plated. A loaf of bread? No, a few slices. And on it goes.

Source: Refinitiv Eikon

Money has fallen in value against these basics more quickly than the general basket of expenses measured by the government. The debasement there has ‘only’ been 60%. Why so much lower? Gains in efficiency should always help to some extent and this period also includes the emergence of China as the top supplier of stuff of all kinds to the world. Cheap stuff. These days China is exporting less consumer goods than it used to because to a large extent it’s already competing with itself rather than undercutting western producers. The wage gap with other countries has narrowed sharply.

Aside from moaning about prices, the harsh lesson is that sitting on cash really isn’t an option at these times. A 1% interest rate on a deposit account barely accounts for the buying power lost in just a month.

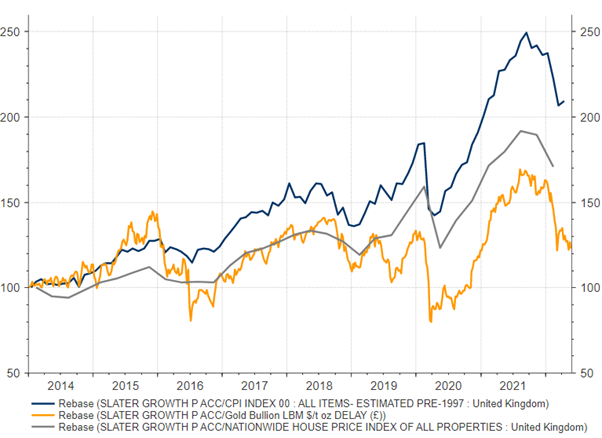

Here is the Slater Growth Fund since 2014 versus the CPI index (in blue), versus gold (in,er, gold) and versus house prices in grey. Gold is a solid store of value but that’s all it is. Gold sleeps while shares live and grow. Central banks exist by grace and favour of governments. They house themselves in impressive headquarters but the reality they simply issue IoUs. Even commercial banks have to prove themselves by lending wisely. Central banks just ‘lend’ to their bosses.

Source: Refinitiv Eikon

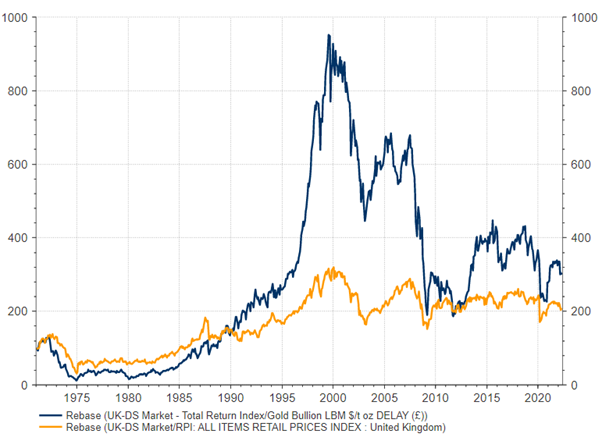

Taking a longer view, in the next chart we compare gold to the UK stockmarket including reinvested dividends. You can see that shares left gold for dead between 1970 and 2000, but then gave some of it back. The compound overall return was 2% per year.

The second line in orange compares shares prices excluding dividends with UK retail prices. Here the return was 1.3%. Inflation data is always suspect but it’s all we have. Gold has been a magnificent asset during the long period of minimal interest rates. If central banks are serious about moving to positive real interest rates, then bullion will face a serious headwind, just as it did after the central banks belatedly started fighting inflation in the 1980s.

A return to honest money with positive real interest rates will be the springboard for higher productivity growth and sustained returns from equities.

Source: Refinitiv Eikon

Risk Warning: Past performance is not necessarily a guide to the future. The value of investments and the income from them may go down as well as up. Investors may not receive back their original investment. The Funds have a concentrated portfolio which means greater exposure to a smaller number of securities than a more diversified portfolio. Charges are not made uniformly throughout the period of the investment. The Funds invest in smaller companies and carries a higher degree of risk than funds investing in larger companies. The shares of smaller companies may be less liquid and their performance more volatile over shorter time periods. The Funds can also invest in smaller companies listed on the Alternative Investment Market (AIM) which also carry the risks described above. The Funds may invest in derivatives and forward transactions for the reduction of risk or costs, or the generation of additional capital or income with an acceptably low level of risk which is unlikely to increase the risk profile of the Funds significantly. This email is provided for information purposes only and should not be interpreted as investment advice. If you have any doubts as to the suitability of an investment, please consult your financial adviser.

The latest Key Investor Information Documents and Prospectus is available free of charge from Slater Investments Ltd and on their website. You are required to read the Key Investor Information Document of the Fund and the Supplementary Information Document before making an investment. Telephone calls may be recorded. Slater Investments Ltd, which is authorised and regulated by the Financial Conduct Authority, is the manager of the Slater Income Fund. Slater Investments Ltd address is Nicholas House, 3 Laurence Pountney Hill, London, EC4R 0EU.

Slater Investments does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this website should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.

Regulatory: Slater Investments Limited is authorised and regulated by the Financial Conduct Authority Registration Number: 165999