PEGwatch was asked to give a view on the outlook for the UK market, more particularly for the type of shares we like to hold in Slater Growth and Slater Recovery.

To discuss this it’s easier to take the UK mid-cap index as a proxy. For starters, below we compare the growth in earnings per share between the UK, in thick blue felt pen, and the US.

The green line shows US earnings in dollar terms and the orange one tracks them in sterling. Lately the dollar has become a petrocurrency and it’s been away with the fairies.

Source: Refinitiv Eikon

The point is that, aside from this recent currency flurry, earnings in London and New York have kept pace very well. In a capitalist system with freely-moving capital, this is what should happen most of the time.

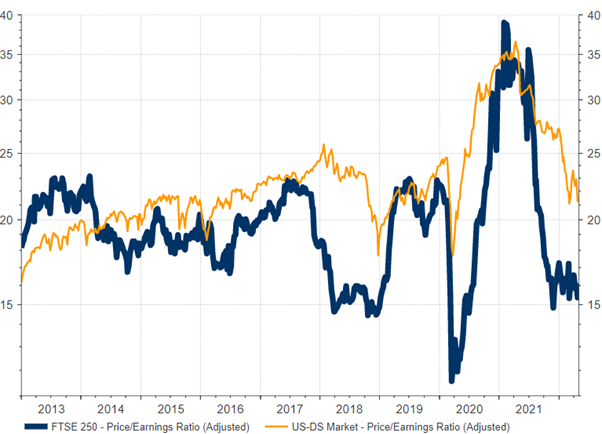

Next we look at the historic Price to Earnings (PE) multiples in London, thick blue again, and New York. The UK has been in the dog house rating-wise since the Brexit referendum. But it seems to have built a floor at around 16x forward. We’ve been in a valuation bear market for five or six years so the risk of further slippage seems quite small. Of course those forecasts may go lower but the market likes to look across the valley, or down the hill. It’s a strange fact of history but recessions are good times to start investing. This is because the authorities start to ease and bad times help to sort out the shining stars from the black holes.

Historic PE of London mid-market shares (in blue) versus US market (in orange)

Source: Refinitiv Eikon

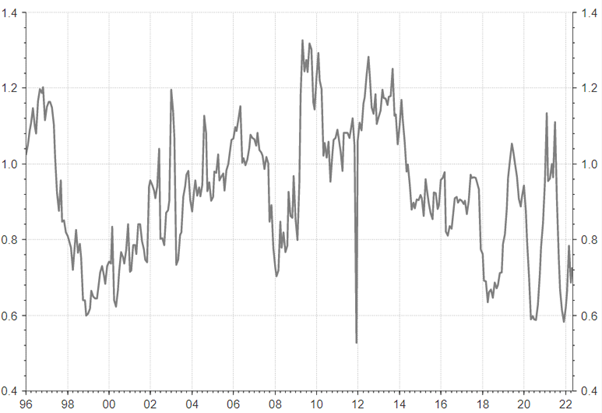

Despite the danger of overloading readers with charts, here we show the relative historic PE multiples. History shows that the UK mid-caps move between 0.6 and 1.3 in relative ratings. Phases of unpopularity are followed by rapid catch ups.

Source: Refinitiv Eikon

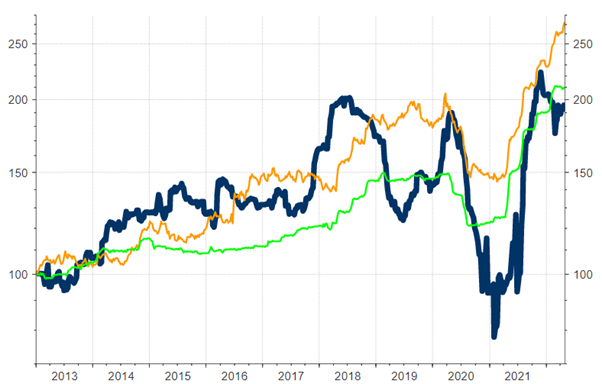

Why do ratings bounce back? Because of profits. The next chart compares earnings growth for the mid-caps to the trend in share prices. The point is the market isn’t walking on air. There’s solid ground out there.

UK mid-cap index versus the growth in earnings.

Source: Refinitiv Eikon

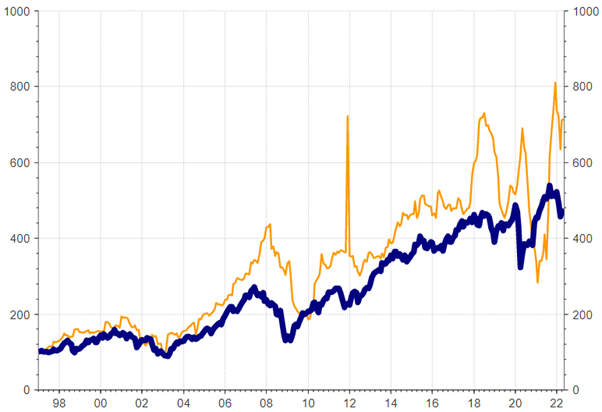

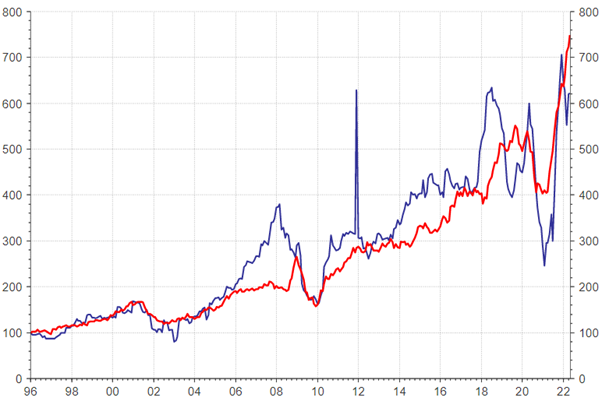

And wrapping up the comparison with the US (orange) and UK (navy), we compare earnings growth between the two markets. Even this chart flatters New York as the recent outperformance has been thanks to the recently acquired petrocurrency status of the dollar.

Earnings growth of UK mid-market companies (in blue) versus New York (in red and converted to sterling)

Source: Refinitiv Eikon

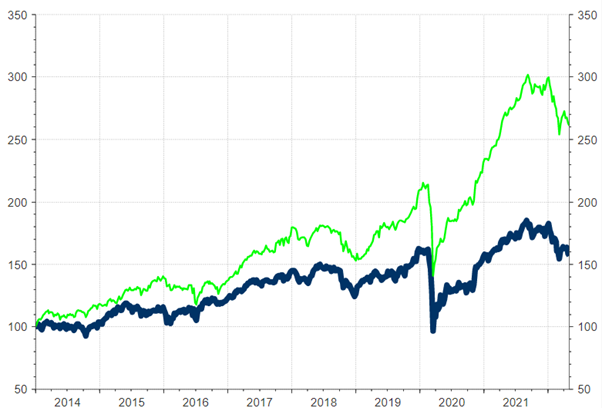

Finally, an advert. Here we compare the total return from UK mid-caps to the returns from Slater Growth (in this case the P shares).

Risk Warning: Past performance is not necessarily a guide to the future. The value of investments and the income from them may go down as well as up. Investors may not receive back their original investment. Please refer to our full Risk Warning below.

Slater Growth Fund compound return (in green) versus UK mid cap companies (in blue)

Source: Refinitiv Eikon

Prices go up and they go down but our pursuit of growth at a reasonable price seems to work pretty well.

The world has been through a plague of frogs lately. It’s necessary to go back to the 1970s to find a decade which has been as trying. The point to hang on to at these times is that capitalism keeps working away in the background despite all the troubling headlines. Profits are the sheep dogs and share prices are the sheep. Sometimes they rush up the hill or down it, but soon enough the sheep dogs send them where they’re wanted.

Risk Warning: Past performance is not necessarily a guide to the future. The value of investments and the income from them may go down as well as up. Investors may not receive back their original investment. The Funds have a concentrated portfolio which means greater exposure to a smaller number of securities than a more diversified portfolio. Charges are not made uniformly throughout the period of the investment. The Funds invest in smaller companies and carries a higher degree of risk than funds investing in larger companies. The shares of smaller companies may be less liquid and their performance more volatile over shorter time periods. The Funds can also invest in smaller companies listed on the Alternative Investment Market (AIM) which also carry the risks described above. The Funds may invest in derivatives and forward transactions for the reduction of risk or costs, or the generation of additional capital or income with an acceptably low level of risk which is unlikely to increase the risk profile of the Funds significantly. This email is provided for information purposes only and should not be interpreted as investment advice. If you have any doubts as to the suitability of an investment, please consult your financial adviser.

The latest Key Investor Information Documents and Prospectus is available free of charge from Slater Investments Ltd and on their website. You are required to read the Key Investor Information Document of the Fund and the Supplementary Information Document before making an investment. Telephone calls may be recorded. Slater Investments Ltd, which is authorised and regulated by the Financial Conduct Authority, is the manager of the Slater Income Fund. Slater Investments Ltd address is Nicholas House, 3 Laurence Pountney Hill, London, EC4R 0EU.

Slater Investments does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this website should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.

Regulatory: Slater Investments Limited is authorised and regulated by the Financial Conduct Authority Registration Number: 165999