All statements made in this article are opinions of the writer(s) and are not to be constituted as advice. Please refer to our full Risk Warning at the end of the article.

Bonds

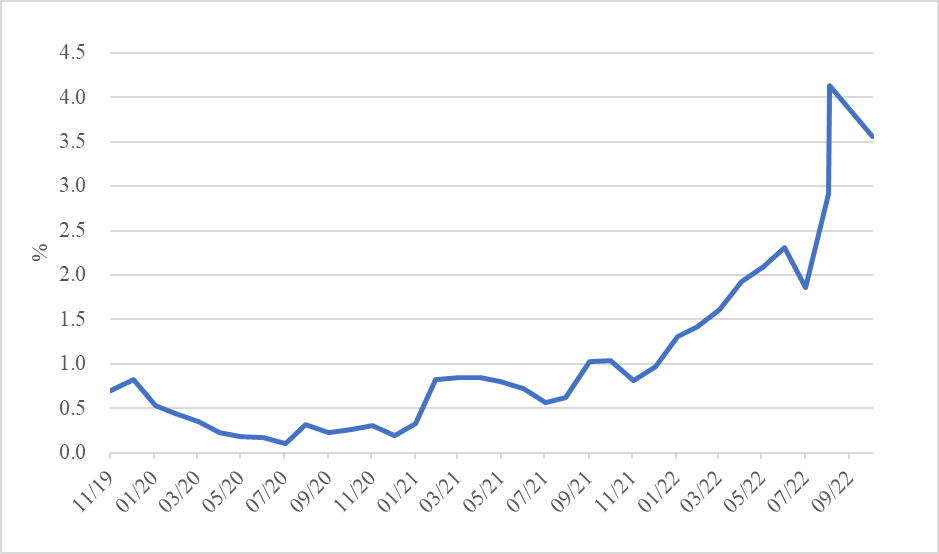

The yield of the UK 10 year gilt has risen from under 1% at the start of the year to nearer 4% now, accelerating especially violently in the last couple of months as concerns about persistent inflation – Kryptonite for bonds – were compounded by the fiscal impurity of the brief Truss government.

UK Ten Year Gilt Yield

Source: Slater Investments Limited

Source: Slater Investments LimitedThis rapid move in the price of money has implications for all asset classes, but what, in particular, does it mean for the UK Equity Income investor?

Ta-ra TINA

As bond yields got ever skinnier in recent years, income-seeking investors looked elsewhere, reversing the traditional paradigm that bonds were for income and equities for growth. The idea grew that There Is No Alternative (TINA) to owning equities. This was, of course, part of the purpose of Quantitative Easing (QE) and yield suppression. As QE now moves to Quantitative Tightening (QT) with Central Banks starting to sell down their huge bond holdings and Central Banks globally hiking policy rates, bond yields are now at a similar level to the yield of the UK Equity market.

This means that income investors now have the appearance of choice. With apologies to Lewis Carroll, we think there are 5 good reasons to prefer Equity Income.

1. Exiting the Rabbit Hole

The current situation is not weird or unusual. Gilts yielding 4% is not in itself unhealthy. What has been weird and unusual is the preceding decade when Central Banks unleased the greatest monetary policy experiment in the history of money. This culminated in large chunks of the bond market trading at negative yields. That was definitely weird and unusual. Like something out of Alice Through The Looking Glass, investors were having to believe six impossible things before breakfast.

2. Was it all just a dream?

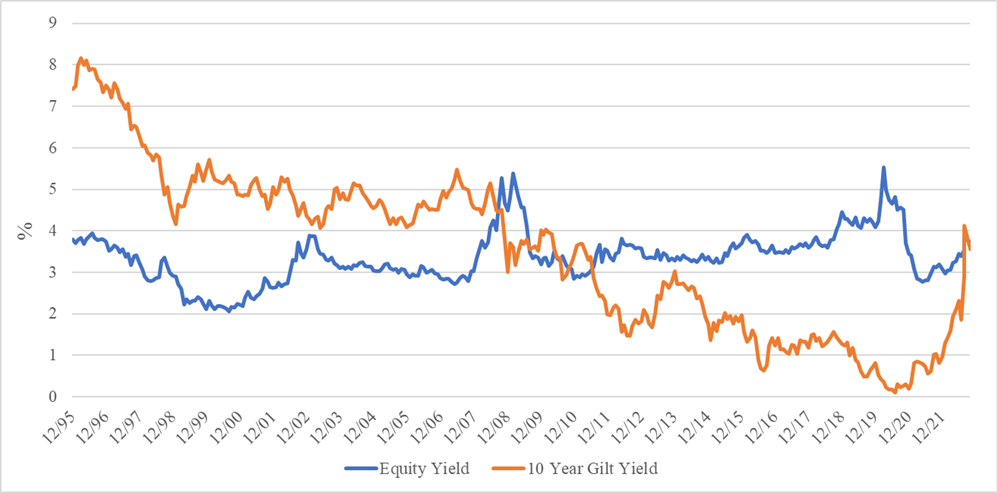

The chart below shows the longer term picture of the UK 10 year gilt yield and the yield of the UK equity market.

UK Equity Yield (Blue) & UK 10 Year Gilt Yield (Orange)

What is interesting is that the equity market, since about 2010, has not “believed” that the plunge in gilt yields was “real.” If equities had chased the bond yield lower, then UK equities would probably be 100% higher. If this had been the case, then equities would indeed be due a tumble. But the UK equity market (perhaps unlike the US) broadly stayed in its long-term range of yielding 3%-4% even as gilt yields headed towards zero. Equities never partook of the state sanctioned potion labelled, “Drink Me”.

The equity market is now trading towards the top of that 3%-4% range, suggesting there is nothing to fear from gilt yields normalising.

3. Bonds should yield more than equities…. “That’s Logic”

Owning a dividend paying equity gives investors the prospect of a rising dividend stream. With the Slater Income Fund, particular focus is on companies that have the best prospects for long-term dividend growth. The coupons paid by a bond are, by contrast, fixed. Which would you rather? Tweedle Growth is better than Tweedle Flat.

4. Mad Hatter’s Tea Party

With inflation at 10% currently and best guesses suggesting it might average 6% in 2023, then real bond yields are still starkly negative. Bond markets are still perhaps in Wonderland.

5. Jam Today

More normal interest rates should reduce the zeal for Jam Tomorrow stocks and bring back investment horizons to more normal levels. Equity Income stocks tend to offer quite high levels of Jam Right Now.

That is certainly the case with the Slater Income Fund, where a carefully selected portfolio of stocks offers a trailing yield of 4.8% with robust prospects for dividend growth.

“Only a few find the way, some don’t recognise it when they do, some…don’t ever want to”

– The Cheshire Cat

Risk Warning: Past performance is not necessarily a guide to the future. The value of investments and the income from them may go down as well as up. Investors may not receive back their original investment. The Slater Income Fund has a concentrated portfolio which means greater exposure to a smaller number of securities than a more diversified portfolio. Charges are not made uniformly throughout the period of the investment. The Slater Income Fund invests in smaller companies and carries a higher degree of risk than funds investing in larger companies. The shares of smaller companies may be less liquid and their performance more volatile over shorter time periods. The Slater Income Fund can also invest in smaller companies listed on the Alternative Investment Market (AIM) which also carry the risks described above. The Slater Income Fund may invest in derivatives and forward transactions for the reduction of risk or costs, or the generation of additional capital or income with an acceptably low level of risk which is unlikely to increase the risk profile of the Funds significantly. This article is provided for information purposes only and should not be interpreted as investment advice. If you have any doubts as to the suitability of an investment, please consult your financial adviser.

The latest Key Investor Information Documents and Prospectus is available free of charge from Slater Investments Ltd and on their website. You are required to read the Key Investor Information Document of the Fund and the Supplementary Information Document before making an investment. Telephone calls may be recorded. Slater Investments Ltd address is Nicholas House, 3 Laurence Pountney Hill, London, EC4R 0EU.

Slater Investments does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this article should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.

Regulatory: Slater Investments Limited is authorised and regulated by the Financial Conduct Authority Registration Number: 165999