All statements made in this article are opinions of the writer(s) and are not to be constituted as advice. Please refer to our full Risk Warning at the end of the article.

Some hedge funds brag about calling turns in the market. They place massive bets on the back of their confidence. George Soros made his famous billion dollar gain from shorting sterling; Michael Burry was lionized in The Big Short. (Repeated shots of somebody staring into the middle distance while he waits for his positions to come good…) Nobody has yet tried to make a movie about the typical day of Nassim Nicholas Taleb, author of the Black Swan. This is not surprising as he bragged in his famous and excellent book that he simply went to the gym rather than waste time watching the screens. He was being honest about the daily life of a fund manager. We leave headbutting the screen to market makers who are feeling tired and emotional. If it was allowed by health and safety, many large brokers would likely hire eunuchs to bang rhythmically on kettle drums and call for ‘ramming speed.’ In fund management there are no kettle drums and serenity reigns. Emotion is the enemy.

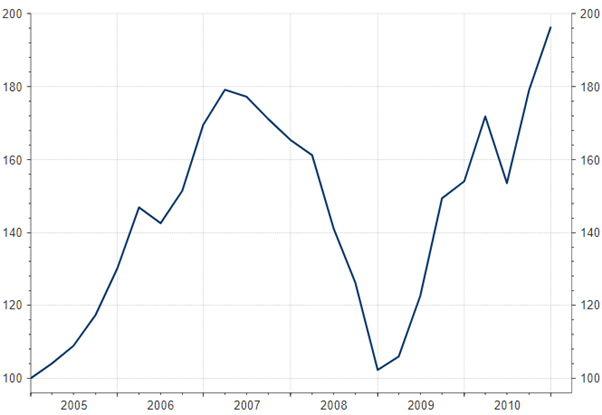

But we do believe in numbers and in what they can tell us. The markets have been pretty volatile lately and the storms don’t show any signs of abating. Quite the opposite. So, in this exercise we looked at four timing strategies to see how well they worked between January 2005 and December 2010. Those six years were not dull. Here is the London mid-cap index (with dividends reinvested) over those six years.

Source: Refinitiv Eikon

You might think: simple, just invest when the market has crashed and make a huge killing. So we compared four strategies:

- £240k up front

- £10k each quarter

- £60k every 18 months

- £240k at the market low at the end of 2008.

To make this more realistic we assumed 3% annual interest on cash which hadn’t yet been invested.

The surprise here is how little difference it made whether an investor bought upfront or somehow managed to time the market perfectly and invest at the low point. There was only a marginal difference between investing each quarter versus every 18 months. During those six years the forward Price-to-Earnings Ratio (PE) on the overall UK market fell from 12.5 to 10.5. That de-rating reduced the benefit to investors from the rise in profits, but it couldn’t blunt it entirely. We might now be in a similar situation where generally rising interest rates will hold back a recovery in PE multiples or even squeeze them a little more. The longer term the perspective, the less the initial price paid matters. Still, it always hurts to buy and then be quickly offside.

When is a good time to buy?

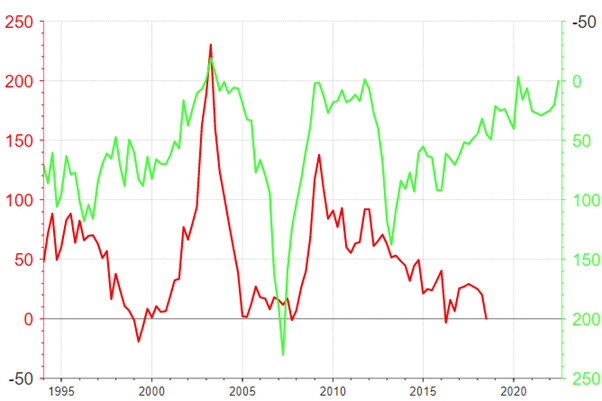

The following charts compare the previous four year’s total return of UK mid-caps with their performance in the following four years. You will notice that a lousy four years, with green at zero, was followed by good returns over the following four years. The 230% gain between 2003 and 2007 was exceptional but the 138% between 2008 and 2012 was pretty good, as was the 92% between early 2012 and early 2016. An investor who had loaded up at those three dates would have averaged a 26% per year total return over the following four years.

Previous four years’ total return (in green – inverted right hand scale) versus the subsequent four-year return (in red, left hand scale)

Source: Refinitiv Datastream

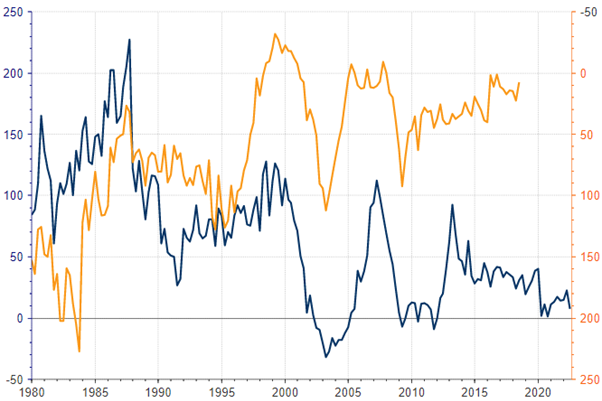

In case you wonder if this pattern is just a quirk of the mid-caps, we can assure you it isn’t. Here is the whole UK market index. It’s a more muted relationship but the correlation is still there.

UK market total return over the previous four years (blue, left hand scale) versus the total return over the following four years (orange, right-hand scale inverted)

Source: Refinitiv Datastream

As we mentioned, the longer the perspective the less it matters when you buy. This is because the driver for share prices in the long term is the increase in company profits. And this growth in turn is due to the steady accumulation of capital in the business which is put back to work each year in greater scale as it builds up.

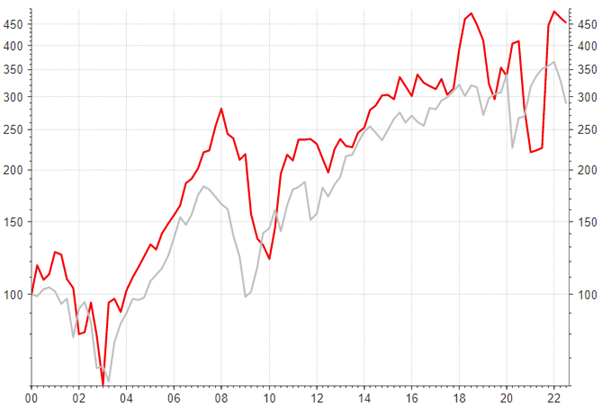

This chart compares UK mid-cap earnings to the mid-cap price index. Earnings are the cause, shares prices are the effect.

This chart compares UK mid-cap earnings (in red) to the mid-cap price index (in grey). Earnings are the cause, shares prices are the effect.

Source: Refinitiv Eikon

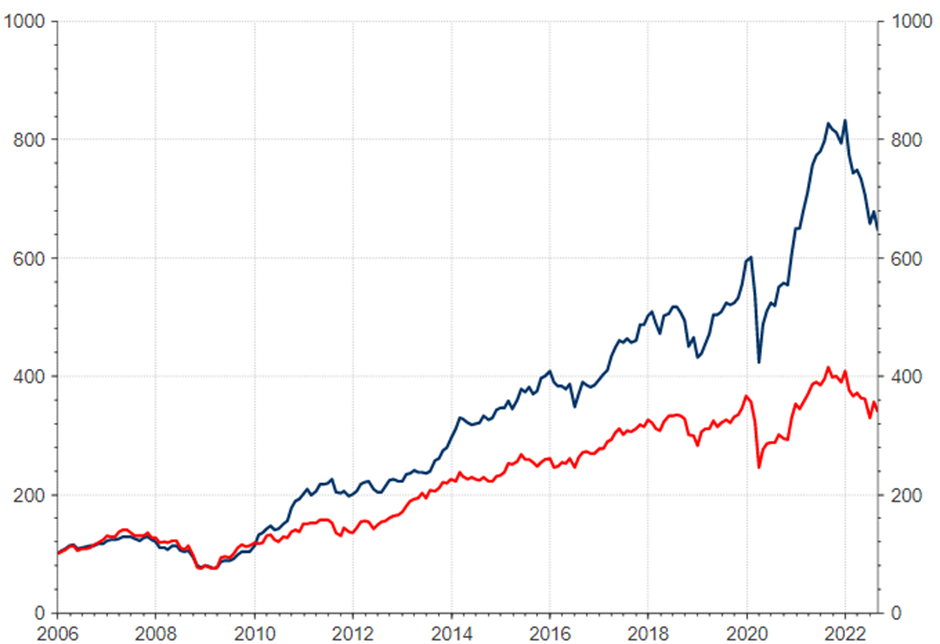

We draw the conclusion from this exercise that mechanically topping up may sometimes not be the best strategy but the longer the period concerned the less difference it will make. The Slater Growth Fund has beaten the market average by a wide margin – as our chart below shows. This is because we focus on lower-rated companies where profits are growing, and re-rating is likely. When times are bad, we just do more of the same, because it works even better.

Slater Growth Fund (in blue) versus UK mid-market companies index (in red):

Risk Warning: Past performance is not necessarily a guide to the future. The value of investments and the income from them may go down as well as up. Investors may not receive back their original investment. Please refer to our full Risk Warning at the end of the article.

Source: Refinitiv Eikon

Risk Warning: Past performance is not necessarily a guide to the future. The value of investments and the income from them may go down as well as up. Investors may not receive back their original investment. The Funds have a concentrated portfolio which means greater exposure to a smaller number of securities than a more diversified portfolio. Charges are not made uniformly throughout the period of the investment. The Funds invest in smaller companies and carries a higher degree of risk than funds investing in larger companies. The shares of smaller companies may be less liquid and their performance more volatile over shorter time periods. The Funds can also invest in smaller companies listed on the Alternative Investment Market (AIM) which also carry the risks described above. The Funds may invest in derivatives and forward transactions for the reduction of risk or costs, or the generation of additional capital or income with an acceptably low level of risk which is unlikely to increase the risk profile of the Funds significantly. This article is provided for information purposes only and should not be interpreted as investment advice. If you have any doubts as to the suitability of an investment, please consult your financial adviser.

The latest Key Investor Information Documents and Prospectus is available free of charge from Slater Investments Ltd and on their website. You are required to read the Key Investor Information Document of the Fund and the Supplementary Information Document before making an investment. Telephone calls may be recorded. Slater Investments Ltd address is Nicholas House, 3 Laurence Pountney Hill, London, EC4R 0EU.

Slater Investments does not offer investment advice or make any recommendations regarding the suitability of its products. No information contained within this article should be construed as advice. Should you feel you need advice, please contact a financial adviser. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment.

Regulatory: Slater Investments Limited is authorised and regulated by the Financial Conduct Authority Registration Number: 165999